The Sustainable Development Goal (SDG) 8 calls for delivering “full and productive employment and decent work” to young people. This requires providing adequate education and training, enhancing access to formal employment, and opening business environments, including access to finance to young people.

In Rwanda, youth unemployment is relatively high at 25.6% among youth population aged 16-30 years as compared to the adults (aged 31 years and above) which is at 17.1%. Nonetheless about 60% of employed Rwandan youth work in nonproductive jobs such as subsistence agriculture, retail, and construction. Basically, Rwanda has a considerable number of unemployed and underemployed youth. The youth unemployment patterns in Rwanda show that 12.2% of unemployed youth have no education, 39.4% have achieved secondary education while 32.4%. are university graduates.

What’s is alarming?

This number of unemployed youth cannot be ignored considering that above 70% of Rwanda’s population are below 35 years of age. If left unchecked it is likely to lead to serious social repercussions including intergenerational cycle of poverty, juvenile delinquency, forced migration, and social unrest.

Youth delinquencies in the country caused by drug abuse, prostitution, alcoholism, informal streets vending, begging and vagrancy is at large in local communities and townships. According to a study on rehabilitation centers conducted by Institute of Policy Analysis and Research-IPAR Rwanda (IPAR), 55% of Rwandan young men at the age of 21 and 43% between 15-18 are either taking or have been taking drugs, while 12.5% of the same age are either engaged or have been engaging in different criminal activities. 76.4% of those who go to rehabilitation centers are Rwandan youth between 18-37 years. So, the dominant age of delinquent behaviors are employable youth who are unemployed.

Prevents youth participation in local governance

Lack of access to employment directly or indirectly seems to disempower Rwandan youth to effectively engage and participate in local governance channels. The research conducted by Never Again Rwanda in 2022, shows that participation of Rwandan youth in local governance channels is still elusive. For example only 39.7% of youth attend national youth council meetings in their local areas, while only 6.5% attend planning and budgeting sessions and only 22.4% attend imihigo sessions in their areas. Moreover, the few who participate are not active enough. According to the same research, of those who attend planning and budgeting sessions, 61.6% have never asked any questions, and 71.7% have never sought feedback on program implementation. 82.3% have never sought feedback on utilization of finances and 87.9% have never questioned potential cases of corruption. The study shows the level of youth indifference in communities.

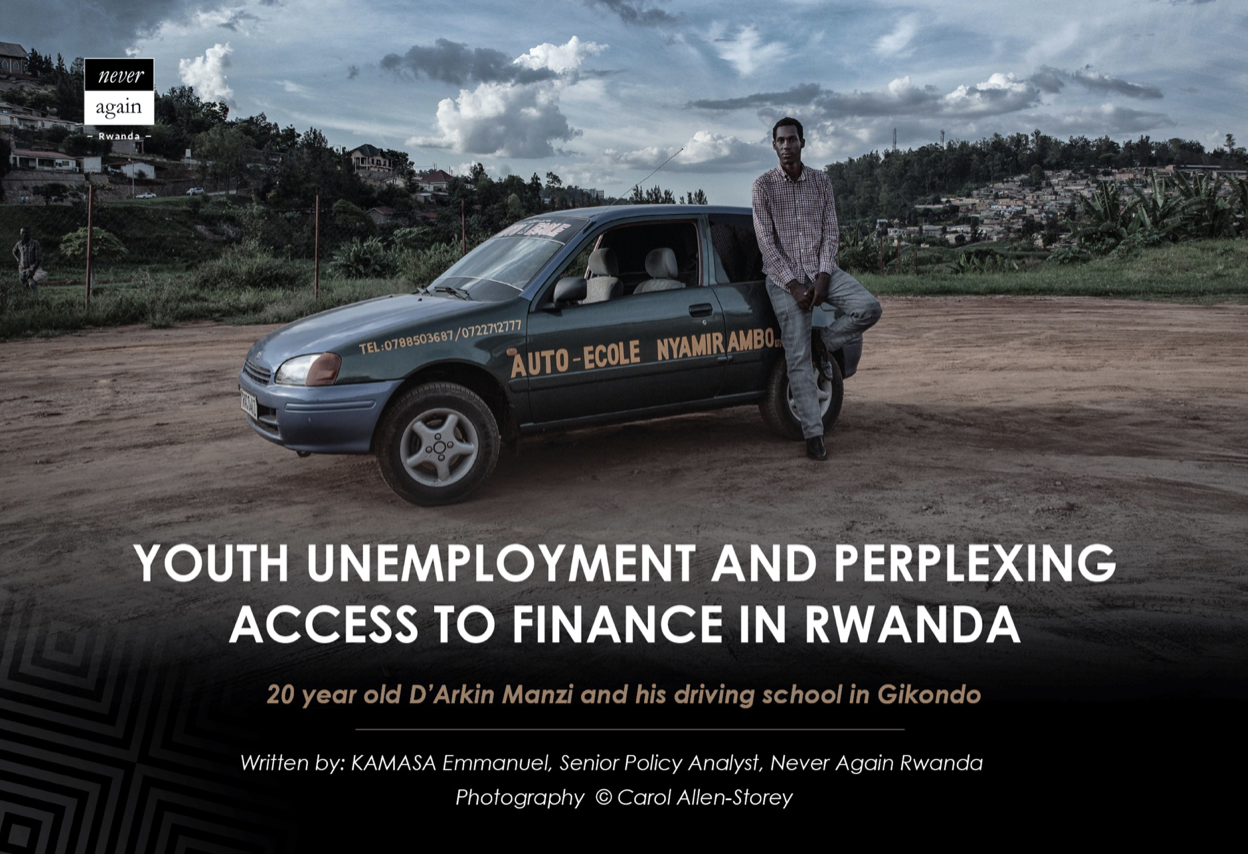

Limited Access to Finance For youth in Rwanda

Youth unemployment is mostly explained by the slow economic growth and other existing macro-economic structures including financial markets in the country that are not able to generate sufficient job opportunities for youth. On the other hand, when young people want to create their own jobs by starting businesses, they often struggle to get access to affordable loans, or loans in general. This is partially due to a lack of collateral. High interest rates also make it difficult for young people to repay their loans on time.

Limited access to finance for unemployed Rwandan youth is baffling, youth startups cannot access finance due to lack of collateral, documentation requirements, unsuitable financial products, risk aversion from financial institutions and lengthy procedures. According to FINSCOPE, 88% of Rwandan youth have access to finance but only 16% have access to credit market. It implies that even though 88% of Rwandan youth have access to finance 84% cannot access any type of credit from any financial institution.

The Business Development Fund

The Government of Rwanda created the Business Development Fund (BDF), a facility established in 2011 to mitigate the fall out between financial institutions and young people mostly the unemployed borrowers, to enable youth and vulnerable groups especially women to access loans from SACCOs, MFIs, banks, and other institutions by covering between 50 to 75 percent of the required collateral. It was a very sounding alternative, however the situation remained corrosive.

The management of BDF admits facing serious challenges to guarantee youth loans because these young entrepreneurs lack working capital and usually have low lender’s trust. Additionally, BDF support comes in after the loan applicant’s project is approved by financial institutions based on their loan requirements which are considered by the youth to be stringent and unachievable.

Policy Alternatives

Access to finance for the Rwandan youth is earmarked by the National Strategy for Transformation (NST1-2018-2024) as a key area of intervention for the government to create decent and productive jobs for the youth. Policy alternatives and interventions are needed for Rwandan youth to access appropriate financial services. It should include developing tailor -made financial tools for young entrepreneurs, such as access to credit and guarantee schemes when they lack collateral. It needs to be a multisectoral endeavor with the public and private sector and CSOs.

Government:

- Government should reform BDF to be able to design a financial facility specifically for youth. BDF needs to go beyond being just a guarantor to the provider of starting capital for youth startups. In collaboration with CSOs, philanthropists and private investors, the government can establish a National Youth Fund (NYF) which would specifically be for youth business financing, providing business advice and mentorship for young entrepreneurs and their projects, Examples can be drawn from other NYFs in other countries like Eswatini Youth Revolving fund, Botswana Youth fund, Tanzania Youth Fund and others.

Private sector

- Private sector should take the lead in supporting young entrepreneurs as young business operators help to sustain a vibrant marketing and supply chain in the national economy.

- Private business, banking, MFIs, SACCOs and Equities should design financial products targeting youth and the businesses they create. Angel investor networks and sources of seed funding could be created to support young entrepreneurs.

- It is likewise important for the private sector to integrate and develop young talents to keep their industries energetic and innovative by streamlining mechanisms of supporting young graduates and school leavers with professional internships, industrial training and part-time jobs.

Civil Society Organizations

- Civil society organizations can play a significant role to enable youth to access employment and finance including among others, designing hands on entrepreneurial mentorship programs focused on enhancing business competencies of school leavers, graduates, and young entrepreneurs. It should be a hands-on and purposeful mentorship to enable young business aspirants to build their business and social networks, access to capital, markets, and supplies.

- CSOs should devise program to support young people to access finance either by providing or mobilizing seed capital through grants. CSOs can also support youth to mobilize business coaching professionals and volunteers to help young people streamline their business projects and undertakings to be able to attract confidence of financing agencies and markets.

reference

- Global indicator framework for the Sustainable Development Goals and targets of the 2030 Agenda for Sustainable Development, https://unstats.un.org/

-

NISR, Labour Force Survey Trends-February 2022(Q1), https://www.statistics.gov.rw/

-

CHARO, R & PRYCE R.S, “Banking on youth: Rwanda’s path to a 21st century economy” March 07, 2022, https://blogs.worldbank.org/

-

Labour Force Survey, Annual Report 2022, National Institute of Statistics Rwanda (NISR), March 2023

-

Pamela Abbott and Florence Batoni,” Disaffected and Delinquent Male Youth in Rwanda: Understanding Pathways to Delinquency and the Role of Rehabilitation and Vocational Skills Training, Institute of Policy Analysis Rwanda, 2011

-

Never Again Rwanda. Research on “Understanding Youth Participation in Local Governance Processes for Decision-Making in Rwanda: Opportunities and Gaps, November 2022,

-

ILO, 2012, National Youth Funds (NYF); Supporting youth to create sustainable Employment Opportunities, Labour Office, Social Finance Programme, Employment Sector. – Geneva: ILO, http://www.ilo.org/publns

-

Azimut, 2022, MSMEs AND ACCESS TO FINANCE IN RWANDA Challenges and way forward, https://azimut-if.com/

-

FINSCOPE YOUTH INCLUSION IN RWANDA 2020- https://afr.rw/

-

Information on Youth Financing shared by BDF to NAR, December 2022

-

U.S. Agency for International Development (USAID) Nguriza Nshore. (2018). Rwanda Banking and Investment Analysis.

-

NST1

-

OECD (2020), Advancing the Digital Financial Inclusion of Youth, www.oecd.org